June 2, 2026

Marvell Gets the Huang Endorsement

What the MRVL Surge Means for Traders Right Now

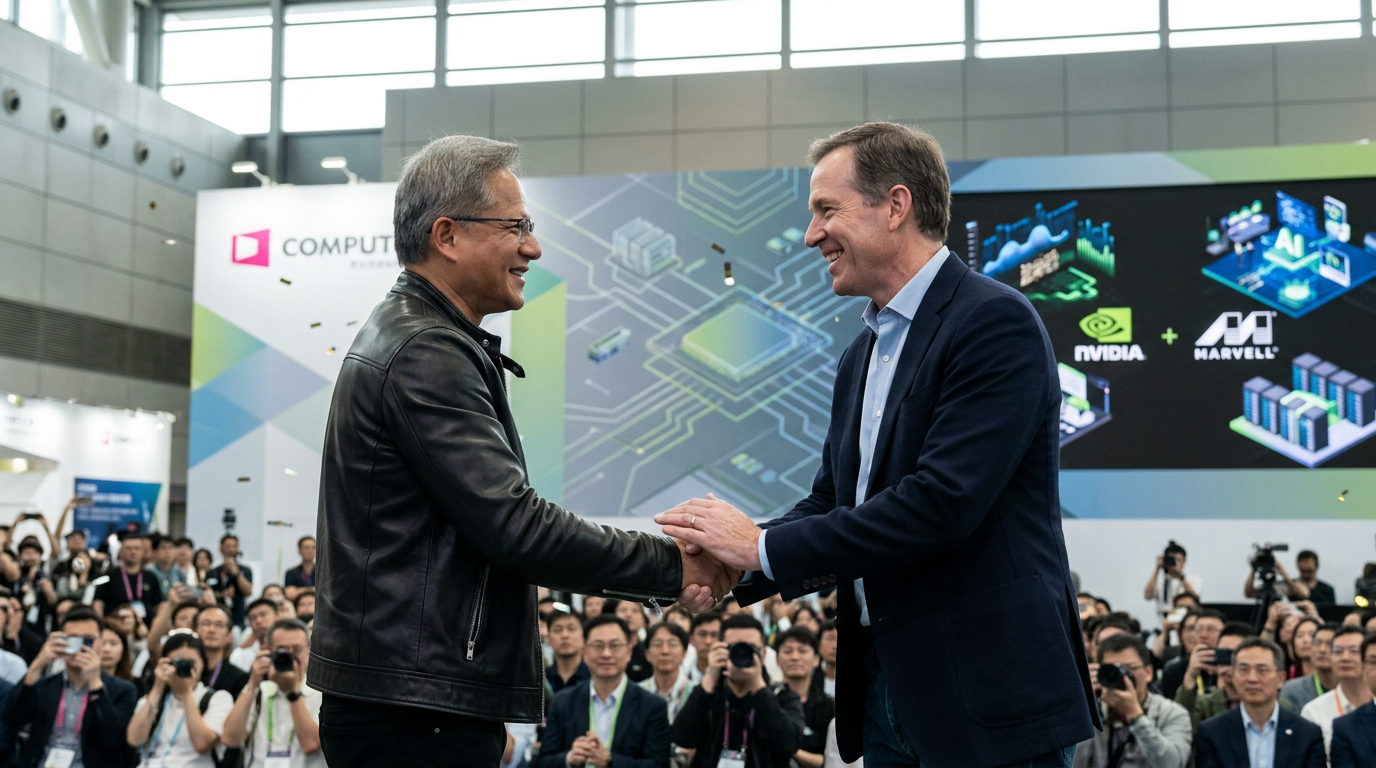

This morning at Computex Taipei, Nvidia CEO Jensen Huang walked onstage alongside Marvell Technology CEO Matt Murphy and said, simply: “Ladies and gentlemen, the next trillion-dollar company.” That was it. That was enough.

Marvell (NASDAQ: MRVL) surged nearly 30% on the session, hitting an intraday all-time high of $277.22, set to add more than $47 billion in market capitalization if gains hold. The tech sector, for context, was up about 0.8% on the same day. This was not a sector move. This was a targeted, high-conviction repricing of one specific company by one of the most influential voices in technology.

Worth noting before we dig in: Huang’s remark was partly playful, delivered during a light exchange with Murphy onstage. But the market heard it as a hard endorsement, and given what Nvidia has already put behind Marvell in terms of capital and strategic commitment, treating it as pure theater would be a mistake.

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change.

The world’s first AI “Mega Computer” – Golden Dawn – will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

The Numbers That Actually Matter

Marvell posted record Q1 FY2027 revenue of $2.418 billion, up 28% year over year, beating analyst estimates of $2.40 billion. Operating cash flow hit $638.8 million in the quarter. GAAP gross margin came in at 52.1%, with non-GAAP gross margin at 58%. These are not speculative growth metrics. These are the numbers of a company with real, accelerating revenue momentum.

Data center revenue hit $1.83 billion in Q1, representing 76% of total company revenue and growing 27% year over year. Two years ago, the data center segment was roughly 50% of revenue. The shift in business mix is structural, not cyclical. CEO Matt Murphy cited “exceptional AI-related bookings” as the primary driver, with custom silicon, optical interconnect, and Ethernet switching all contributing.

Forward guidance is where things get genuinely interesting. Management guided Q2 revenue to approximately $2.70 billion, ahead of the $2.60 billion consensus at the time. Full-year FY2027 revenue is now expected to grow approximately 40% year over year to nearly $11.5 billion, up from earlier guidance of 30% growth. FY2028 guidance was raised to approximately $16.5 billion, a $1.5 billion increase from the prior quarter’s outlook. The company has also previously projected its custom chip business could generate more than $10 billion in annual revenue by fiscal 2029.

Why Connectivity Is the Trade Right Now

Murphy’s own comments at Computex deserve equal attention. He argued that as AI infrastructure evolves, the next major bottleneck is no longer compute or memory capacity. It is connectivity. The ability to move enormous volumes of data efficiently between chips and servers, across data centers, at scale. That is the exact problem Marvell’s optical interconnect and custom silicon portfolio is built to solve.

As AI clusters scale from 10,000 to 100,000 accelerators, data transmission efficiency becomes the binding constraint on total system performance. Marvell is the second-largest vendor of networking and optical interconnect solutions in this space. Huang’s own comments emphasized the critical role of data transmission in AI’s full commercialization cycle, which is precisely the infrastructure layer Marvell occupies.

Nvidia has backed this thesis with $2 billion in a strategic investment in Marvell, with the two companies engaged in deep collaboration via the NVLink Fusion platform to develop silicon photonics technology and advance next-generation AI infrastructure. That capital commitment preceded today’s public endorsement by several months. The market is now catching up to what Nvidia already committed to in writing.

This Pre-IPO Stock is Up 4,000% Already

Most people think AR and VR are still years away from mainstream adoption.

But more than 1.5 million professionals are already using one platform to work, collaborate, and replace traditional monitor setups.

Now the company behind it is preparing for its next phase of growth.

With partnerships involving Meta, Qualcomm, and Samsung, plus a new headset already drawing significant demand, some investors believe this story is just getting started.

Sector and Competitive Context

For competitive perspective: Broadcom (AVGO) remains the scale leader in custom AI silicon, posting quarterly revenue of $22.12 billion in the quarter ended April 2026 against Marvell’s $2.42 billion. AMD posted $9.92 billion for the same period, driven by GPU-accelerated data center work. Marvell is not competing dollar-for-dollar with either of those companies on volume. What it is doing is carving out a structurally differentiated position in optical interconnect and custom ASIC development that serves cloud hyperscalers looking for alternatives to off-the-shelf solutions.

Cloud service providers expanding AI-focused data center capacity are increasingly demanding custom-designed semiconductors tailored to specific AI workloads. Marvell has positioned itself as a key supplier in exactly that trend. That is the business model driving the data center revenue concentration, and it is not slowing down.

On a year-to-date basis, MRVL has climbed approximately 130% heading into today’s session, with a roughly 254% gain over the trailing twelve months. The stock hit a new all-time high this morning.

Valuation Tension

The trillion-dollar framing is exactly that: framing. Marvell’s current market cap sits around $240 billion post-surge, still more than four times below the trillion-dollar threshold. Getting there requires the stock to multiply from here by a factor of more than four. That is not a short-term call. It is a long-arc thesis about where AI infrastructure spending flows over the next several years.

Wall Street’s current positioning: 41 analysts cover MRVL, with 31 buys and 8 outperforms. The street mean target sits near $223, which was already close to the pre-surge price. Expect a wave of price target revisions in the coming days. TIKR’s mid-case model points to approximately $490 by January 2031, implying roughly 19% annualized returns from pre-surge levels. The near-term multiple is rich. The multi-year revenue ramp is real. Both things can be true simultaneously.

Technical Structure

MRVL opened with a sharp gap higher and set a new all-time high at $277.22 intraday. Volume is running well above average, which confirms institutional participation in the move rather than retail-driven noise. Gap-up days of this magnitude on record volume tend to establish new support ranges that traders reference for weeks following the session.

Key levels to monitor: The prior all-time high becomes the first reference point for support on any pullback. VWAP for the session will be a real-time indicator of whether large buyers are defending the move or taking gains into strength. A close well above the prior resistance zone would confirm the gap is being absorbed cleanly, not sold into.

Momentum indicators on the daily and weekly charts have moved into extended territory. That does not mean the move is over. It does mean chasing into the close of a 30% gap day carries asymmetric risk relative to waiting for a more defined entry level.

Everyone is focused on SpaceX.

Jeff Brown says they’re missing the bigger story.

After following Elon Musk’s companies for years, Jeff believes a new AI initiative could become one of the most important projects Musk has ever been involved with.

Most investors haven’t paid much attention yet.

That’s exactly why he’s discussing it now.

Three Scenarios From Here

- Bull Case: Gains hold, price targets are revised sharply higher across the street, and Marvell’s FY2027 revenue trajectory toward $11.5 billion is treated as a floor rather than a ceiling. Hyperscaler AI capex continues to expand aggressively, driving demand for both custom silicon and optical interconnect at accelerating rates. MRVL tests $300+ in the near term and builds a base above $260 on consolidation.

- Base Case: Today’s move is partially faded over the coming sessions as traders harvest gains from a 30% single-day move. MRVL consolidates in the $245 to $265 range, supported by strong Q1 fundamentals and the Q2 guidance beat. The medium-term thesis remains intact as the NVLink Fusion collaboration and AI data center spending cycle play out through FY2028.

- Bear Case: The Huang comment is reframed as offhand rather than a formal strategic declaration, and the gap fills partially on profit-taking. If broader tech sentiment deteriorates, MRVL could retrace toward the $220 to $230 zone. The fundamental thesis does not break in this scenario, but the entry risk for latecomers is real. Watch for Nvidia to either reaffirm or stay quiet on the trillion-dollar framing in the days ahead.

What Active Traders Are Watching

First: end-of-day close relative to VWAP. A strong close above VWAP on high volume signals that buyers absorbed supply and controlled the session. A weak close below VWAP suggests the gap was used as an exit by institutional holders.

Second: options market activity. Implied volatility will be elevated given the gap. Premium sellers and defined-risk structures become more attractive when IV is this high relative to historical norms. Directional options plays carry elevated premium risk on a day like today.

Third: analyst response. The mean street target of $223 is now materially below the current price. Price target revisions will follow, and the cadence and magnitude of those revisions will set the tone for institutional flows over the next two to four weeks.

Slight tangent, but it is relevant: Murphy’s framing of connectivity as “the next AI bottleneck” is a broader market signal beyond just MRVL. Companies in the optical networking and silicon photonics supply chain, including Coherent Corp (COHR) and others in the co-packaged optics space, are worth watching in this environment. The infrastructure thesis is wider than one stock.

The honest read here is that Marvell earned this moment. The Q1 revenue beat, the FY2028 guidance raise to $16.5 billion, the $2 billion Nvidia investment, the NVLink Fusion collaboration, the structural shift in data center revenue mix to 76% of total, all of that existed before Huang said anything this morning. What today added was visibility. The question traders need to sit with is not whether the thesis is real. It clearly is. The question is what you are paying for it right now, and whether the risk-reward of a 30% gap day into an all-time high fits your framework.

Preparation over prediction. That is what separates traders who use moments like this from those who get used by them.

For informational and educational purposes only. Not investment advice. Trading involves risk, including loss of principal.