May 5, 2026

VSE Corporation Just Hit $1.1B in Aviation Revenue — Here’s What Traders Need to Know

VSEC Is Not a Household Name – But Its 41% Growth, Expanding Margins, and Pending $2B Acquisition Tell a Compelling Story

A Pure-Play Aviation Story Still Flying Under the Radar

Most investors chasing defense and aviation exposure default to Lockheed Martin or Raytheon. Understandable. But some of the most interesting setups right now are happening several tiers below those primes – in the specialized aftermarket infrastructure that the entire aviation ecosystem depends on to keep flying.

One name that deserves serious attention is VSE Corporation (VSEC), a mid-cap aviation aftermarket distribution and MRO services company headquartered in Miramar, Florida. With a market cap in the range of $4.5–5 billion as of early May 2026, VSE is not a micro-cap sleeper – but it is still well below the institutional radar screens that light up for the primes. That gap may be exactly where the opportunity lives.

What VSE Actually Does Now

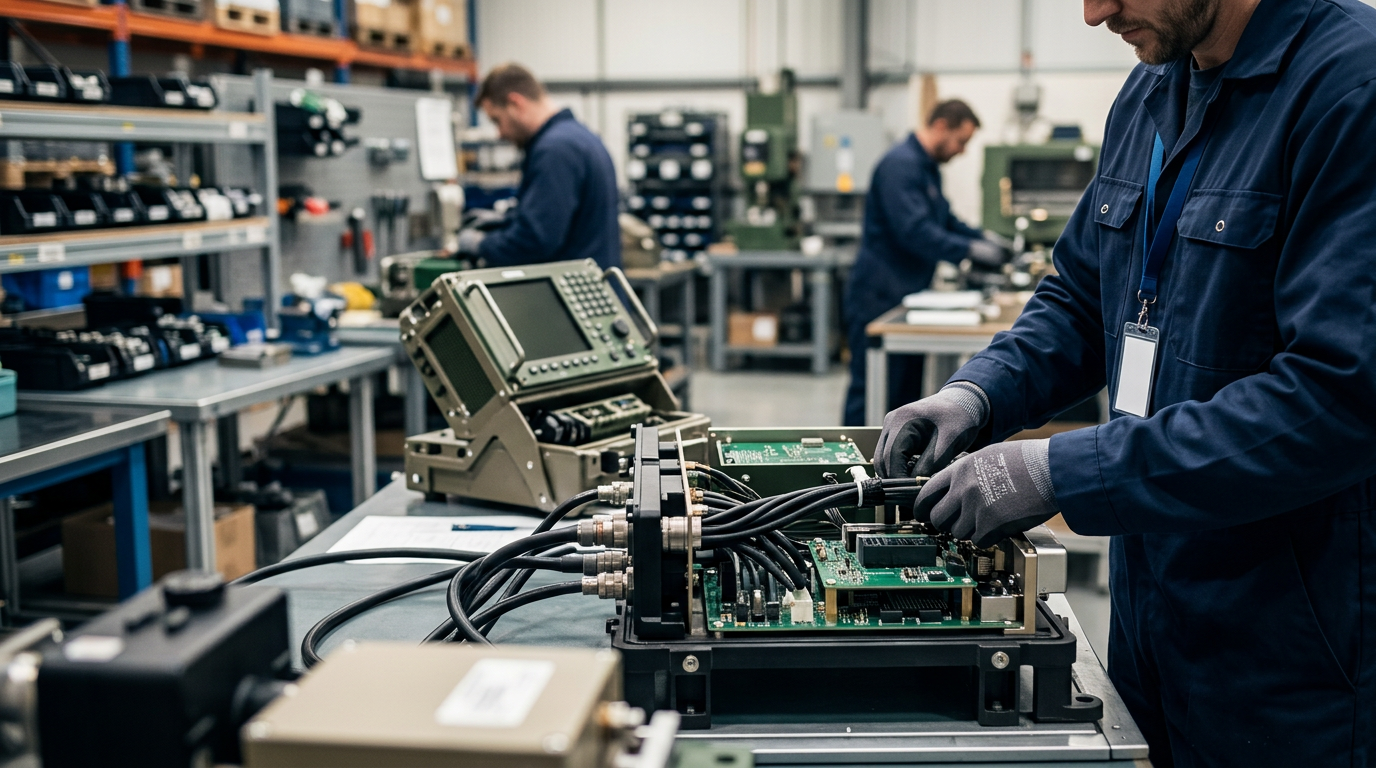

VSE completed a significant strategic transformation in 2025. After divesting its Fleet segment – Wheeler Fleet Solutions – to One Equity Partners in April 2025 for up to $230 million, the company is now a pure-play aviation aftermarket business. No more government vehicle fleets, no more USPS contract exposure. Just aviation.

The company provides aftermarket parts distribution and maintenance, repair, and overhaul (MRO) services for engine components and airframe accessories, serving commercial airlines, regional carriers, business and general aviation operators, and defense clients globally. It is a sticky, asset-light model built around long-duration OEM distribution agreements and specialized repair capabilities that are genuinely hard to replicate at scale.

The Cross-Chain Giant Set for 1,000%+ Gains

As crypto markets surge post-tariffs, one multi-chain financial protocol is being targeted for massive institutional investment before retail discovers it. Its transaction volume is skyrocketing across all major blockchains while its price remains suppressed as retail has yet to discover it – creating a coiled spring ready to release.

Breaking: Access our urgent research on this cross-chain opportunity for just $3!

The Numbers That Actually Matter

Here is where it gets interesting. VSE’s full-year 2025 aviation revenue hit $1.1 billion – a milestone the company had never crossed before – representing 41% year-over-year growth. Distribution revenue led the charge, up 46% to $704 million, while MRO services grew 35% to $408 million. This was not a one-quarter pop. The growth ran through all four quarters of 2025.

- Full-year 2025 Adjusted EBITDA: $182.9 million, up 56% year-over-year

- Adjusted EBITDA margin: approximately 16.5–17% for the aviation segment – a meaningful step up from prior-year levels

- Adjusted net leverage ratio: approximately 1.1x at year-end 2025, reflecting disciplined balance sheet management post-Fleet divestiture

- Full-year 2025 diluted EPS from continuing operations: $2.52, up 133% year-over-year

- Adjusted EPS: $3.92, up 87% year-over-year

The gross margin story has also improved materially. Aviation segment Adjusted EBITDA margins ran in the 17% range for full-year 2025, with management guiding 2026 consolidated Adjusted EBITDA margins of 16.8% to 17.3% – even before fully incorporating the pending Precision Aviation Group acquisition, which carries EBITDA margins above 20%.

The Pending Acquisition – And Why It Changes the Scale Conversation

On January 29, 2026, VSE announced a definitive agreement to acquire Precision Aviation Group (PAG) for approximately $2.0 billion. PAG is projected to generate roughly $615 million of adjusted revenue for full-year 2025 with an adjusted EBITDA margin above 20%. The transaction is expected to close in Q2 2026, pending regulatory approvals.

Slight tangent here, but it matters: VSE funded the PAG deal largely through equity – raising approximately $1.7 billion through public offerings between late 2025 and early 2026. That is significant dilution. Shares outstanding have expanded materially. Any valuation framework built on pre-dilution share counts is already stale.

The combined entity, post-close, would give VSE a much broader footprint in business, general aviation, and rotorcraft markets – segments that often move on different cycles than commercial aviation. Diversification of end-market exposure is part of the thesis here, not just scale.

Why the Story Is Accelerating Now

Global MRO spending is projected to exceed $115 billion annually by 2028, and VSE’s expanding distribution network positions it to capture a growing slice without the capital intensity of an OEM. The company’s OEM-authorized distribution agreements – including expanded partnerships with Pratt & Whitney and Eaton – create barriers to entry that are often underappreciated in screens that focus only on top-line multiples.

Defense sustainment is also a growing contributor. VSE signed a long-term agreement with V2X, Inc. in 2025 to provide repair and overhaul services for engine fuel control units on the U.S. Navy’s TH-73 Thrasher helicopter fleet. That is the kind of contract that adds durability to the revenue base without requiring capital cycle timing.

Management guided full-year 2026 organic revenue growth of 19% to 23% – and that guidance explicitly excludes the PAG acquisition, which is expected to add substantially to the top line once closed.

China Thought They Had This Locked Up

China controls 98% of the world’s gallium supply – critical for modern technology.

But a small American firm may have just changed the game with a breakthrough called GaN.

Watch this presentation to learn how it could reshape tech – and why investors are watching

Risks Worth Knowing

The PAG acquisition is the central execution risk. At $2.0 billion, the deal represents a purchase price approaching the company’s entire market cap heading into the announcement. Goodwill and intangible assets already totaled $937 million – roughly 46% of total assets – before PAG closes. Any integration stumble, or failure to realize synergies, could pressure the multiple quickly.

Customer concentration is also worth flagging. A single affiliated customer group accounted for approximately 20% of 2025 revenue, up from 14% in 2023. That is a meaningful concentration risk that has been building quietly.

Free cash flow generation was modest in 2025 – only $6 million for the full year – as working capital absorbed growth. Inventory expanded 28% to $554 million. These are not crisis metrics, but they are worth monitoring as the company scales into the PAG integration.

Scenario Framework

Bull Case: PAG closes cleanly in Q2 2026, synergies track toward the $15M+ annualized target, combined revenue approaches $1.7B+ on a run-rate basis, and EBITDA margins expand above 17% on the combined platform. Analyst consensus price targets in the $220–270 range would look conservative in this scenario. Re-rating toward a 20–22x EBITDA multiple is possible if execution is clean.

Base Case: PAG closes on schedule with modest early integration friction. Combined 2026 revenue grows 30–35% pro forma. EBITDA margins hold in the 17–18% range. Shares consolidate in the $160–200 range while the market waits for free cash flow improvement post-close. This is the most probable near-term path.

Bear Case: PAG integration runs into delays or margin disappointment. Customer concentration risk materializes. Free cash flow remains negative through 2026. In this scenario, the equity overhang from dilution becomes a headwind, and shares could revisit the $110–120 range – the lower end of the 52-week band. Goodwill impairment risk would become a live conversation.

Active Trader Framework

VSEC has been volatile – 19 moves greater than 5% over the past year, per market data. The 52-week range spans from roughly $110 to $232, which is a wide band that reflects the transformation narrative and deal uncertainty. Current price in the $165–175 area puts the stock well off its highs but meaningfully above the lows.

- Key levels to monitor: $160 (prior support / lower range), $185–190 (near-term resistance), $220+ (bull case re-rate zone)

- PAG close confirmation will likely be the next major catalyst – watch for Q2 2026 announcements

- Volume patterns around earnings (May 5, 2026) will clarify whether institutional positioning is building or reducing ahead of the integration phase

- Options implied volatility tends to spike around catalysts – position sizing should account for gap risk in either direction

The Bigger Picture

VSE is not trying to build the next fighter jet or win the next major defense prime contract. It is building the aftermarket infrastructure that keeps existing fleets flying – commercial, business, defense. In an aviation environment defined by aging fleets, deferred maintenance backlogs, and an MRO capacity shortage, that positioning carries real durable value.

The market, at current multiples, is pricing in execution risk around PAG. That is fair. But if the integration tracks, this is a business generating $1.1B in revenue today with a path to $1.7B+ pro forma – and margins that are expanding, not contracting. The question is not whether the story is real. The question is whether the execution will be.

For informational and educational purposes only. Not investment advice. Trading involves risk, including loss of principal.